The ETF Lyxor CST (Materials & Construction Europe) created in 08/2006 is listed in Euro on Euronext and seeks to replicate the Stoxx600 Net Return Construction & Materials index composed of 20 European stocks including 35% outside the Euro zone, which implies a risk mainly related to the EURO / SEK and EURO / CHF parity.

The fees of this ETF are 0.3% and the AUM of approximately € 36m. Replication is indirect (via Swap) and there is a dividend capitalization policy.

Alternative ETFs: EXV8 (iShares in Euro)

Index & components

This index includes 20 stocks, specialized in the construction market through the cement and aggregates manufacturers such as Lafarge, CRH or Heidelberg, but also manufacturers specializing in building materials such as Saint-Gobain, as well as construction companies that can at the same time being engineering firms and dealers as Vinci, Ferrovial or Eiffage. It should be noted that the first 4 stocks (Vinci, CRH, Saint Gobain and LafargeHolcim) alone represent almost half of the capitalization of the index (47%), which is focused on European companies but whose activities are very international and for certain holdings (as CRH) includes a strong presence in the United States, while others have exposure in the emerging markets (ex: LafargeHolcim).

The construction sector was particularly affected by the financial crisis and then the Eurozone crisis between 2008 and 2012, because it is an activity that depends mainly on financing, whether for infrastructure (public authorities) or for the residential sector. The construction index seems to be gradually picking up in Europe, with the increase in building permits but still waiting for a frank recovery in Europe as growth is accelerating (2.3% estimated for 2018 in the Euro Zone), while housing construction needs are also very significant.

The outlook for the sector is now more favorable, with a recovery that is strengthening and spreading in Europe, interest rates that remain low and stable and large-scale domestic projects like Greater Paris which will represent more $ 30 billion in infrastructure investment, while in the US Donald Trump seems to have not given up on its infrastructure program, including its border wall with Mexico even though it is becoming less and less likely.

Most of the growth in the sector is expected to be in the major regions of the world outside Europe, with interesting prospects in India and Africa in the medium term. China is seen as a separate market for cement-monopolized by highly competitive local price players-and hardly addressed by Western multinationals.

Latest developments

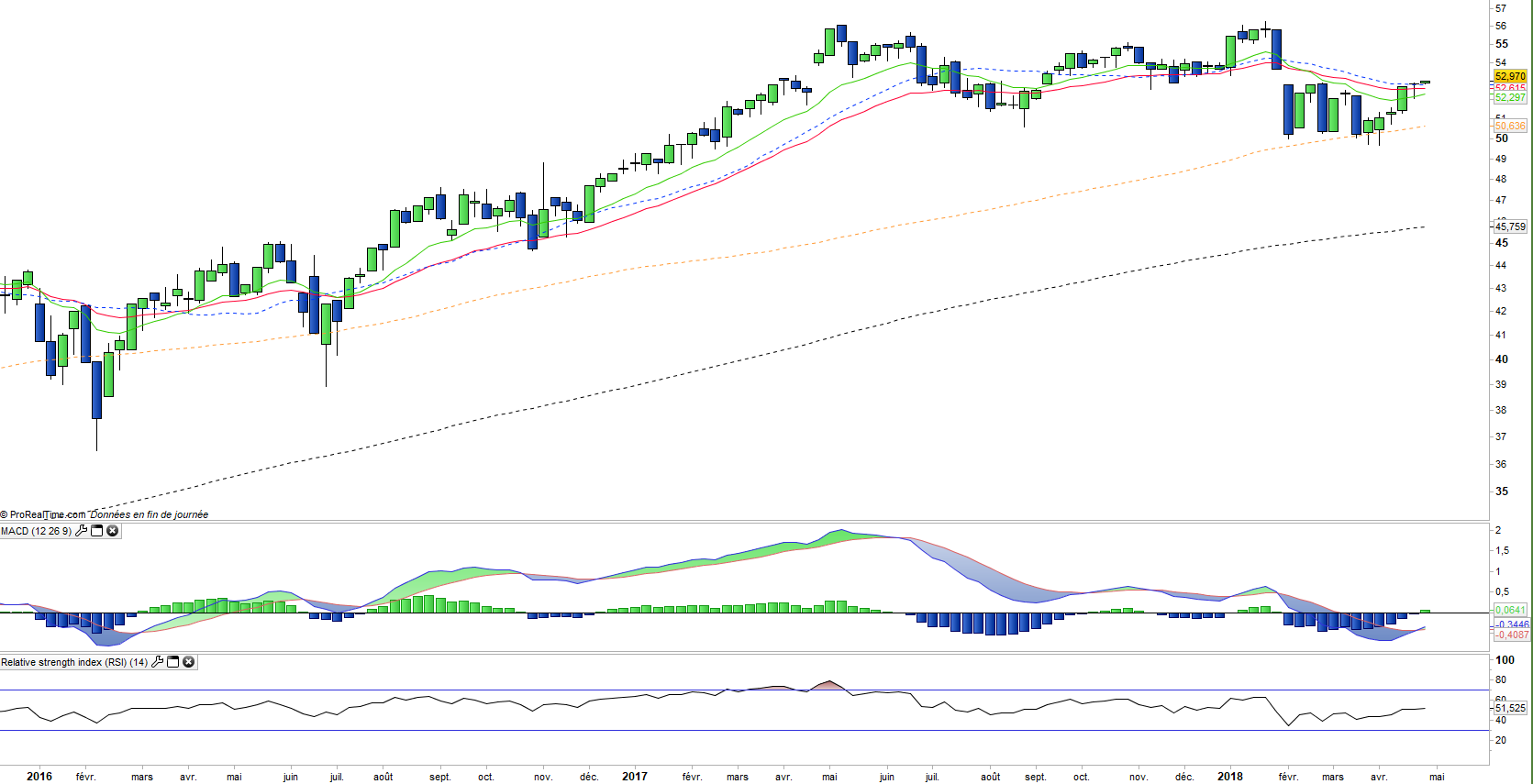

The sector's performance has been positive since 2012 (end of the crisis), and CST rose by 10.5% in 2017 in line with the performance of Stoxx600 and is down -1.3% in 2018 which corresponds to the correction coming from the United States and which has hit the European markets in February and March.

The outlook for large construction groups is generally encouraging for 2018, while European growth should accelerate and have a strong impact on industrial capacity utilization rates which are at a historically low level due to a surplus capacity, therefore the rise in utilization rates in 2018 should be beneficial for margins.

The evolution of oil prices remains to be watched, as the cement industry is one of the biggest consumers of fossil energy. A further rise in oil prices, which are now at 2-year highs ($ 68) potentially linked to new tensions with Iran, would penalize the margins of the cement and construction companies.

The bullish reversal of Vinci (18.6% of the index) and CRH (9.9%), explain in part the better performance of the index in recent weeks.