It should be noted that the 10 main holdings (which represent about 55% of the index) belong to very different sectors, unlike the DAX (overweight in industrial stocks) or the FTSE100 (pharmacy and financials), the CAC40 is indeed more composite in its sectoral composition. However, three high-weighted stocks, Total (10%), LVMH (7.8%) and Sanofi (6.6%) and can influence the index according to their own fundamental factors, which represents a bias.

From a sectoral point of view, we can see that the consumer goods sector represented by luxury goods and cosmetics such as LVMH or Loreal, is one of the most important for the index (18%), just behind industry (19.4%), financials (11%) and energy (11%).

The CAC40's stocks are often world leaders with a very international exposure, and little dependence on the domestic market and with a strong sensitivity to the US Dollar.

French growth remains positive, but above all international investors have regained confidence with the election of Mr Macron, liberal and pro-European. The positive impact on French growth linked to hopes for structural reforms as well as the drop in corporate and capital taxes voted in 2018 are still far from being integrated. France is still in the middle of the cycle, and strong, positive trends could this time trigger if reforms continue.

The medium-term potential of the index is high, but remains hindered for the moment by international problems (trade war, EDF) and European problems (Brexit and Italy) and for some time by internal social unrest (yellow vests).

The improvement of financials is key, but seems to be delayed in time due to the policy of the ECB that will wait until 2019 to normalize its monetary policy, because linked to the gradual rise in long-term rates with the resumption of growth and expectations of inflation, as is already the case in the US, and a more favorable political context.

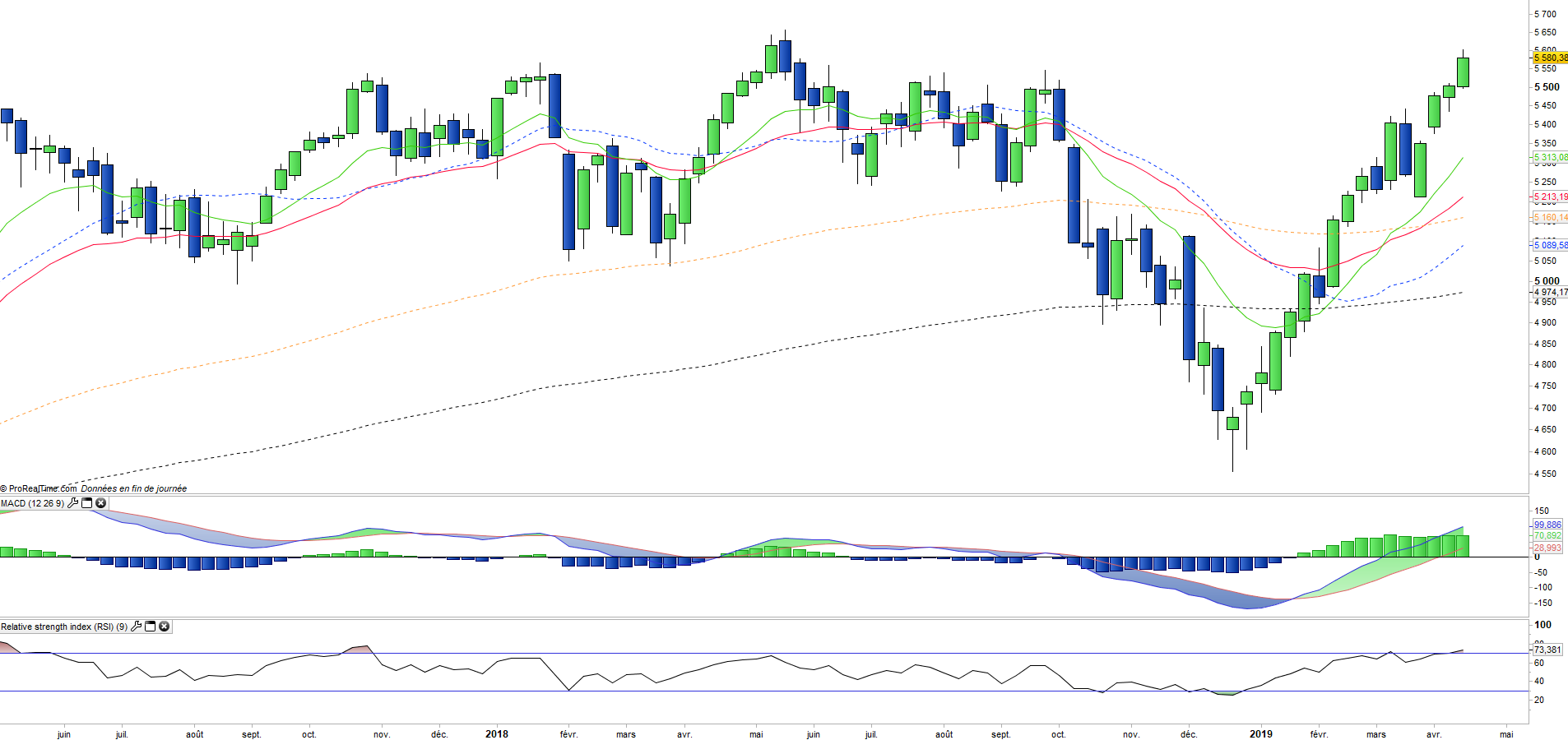

In 2017, the CAC40 achieved a performance of 9.3% which was more than offset by a -11% in 2018. As on the other European or North American indices, the decrease is mainly due to the fall of the markets started from October against the backdrop of a trade war between the US and China, a rate hike policy considered too aggressive by the FED, and more specifically for France, the fear of stopping reforms because of the social protest which is amplified at the risk of destabilizing the government. Since January 2019, the index is rebounding (+ 18%), due to hopes of trade agreements and a more accommodating EDF, but also results of companies less bad than expected and adjustments of earnings outlook for 2019 for the moment quite limited.

Instruments: CAC (Lyxor in Euro), C4D (Amundi in Euro), E40 (BNP in Euro)