The top 10 stocks are mainly large industrial stocks such as Siemens or Bayer, while there are only 2 financial stocks in the DAX: Allianz and Munchener Rueck, the German master index is relatively small and mostly composed of large industrial groups.

Unlike the English, French or Italian indices, the DAX is also distinguished by the absence of large oil companies that weigh heavily in the weighting of the CAC40, FTSE100 or FTSEMIB40, which is double-edged according to the cycle specific to energy sector.

In addition, the financials weigh only 16% of the index, more than half for the insurance giant Allianz, so the banking sector has a low weight reflected in the well-known weakness of Deutsche Bank and Commerzbank. Conversely, the automotive and chemical sectors are heavier than the other European indices, while the technology sector is mainly represented by SAP (9.5%) whose market capitalization exceeds € 130 billion.

In summary, the DAX is a fairly strong index from a sectoral point of view which can make it evolve differently from other European indices. German fundamentals remained solid (historically low unemployment rate at 5.5% and accelerated deleveraging up to 2020) but growth is falling sharply and the economy risks to enter into recession. The main risks concern Germany's main customers, namely the United Kingdom, which could suffer from Brexit, the US in political uncertainty and threatening it with a trade war, Russia which remains a difficult and aggressive neighbor and China because of its commercial practices which also tend to limit access to its domestic market to Western industrialists, particularly in the automotive and technology sectors.

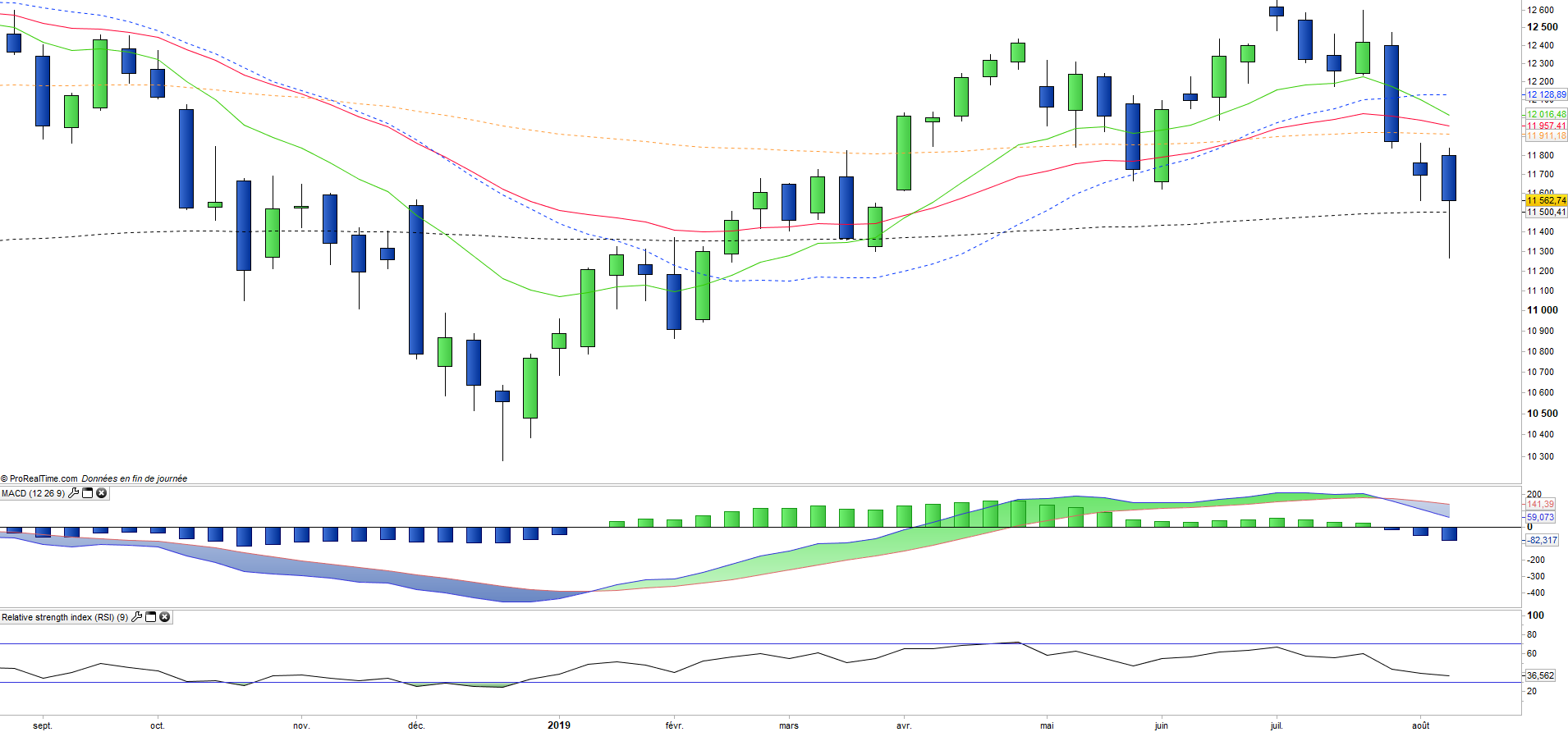

After an increase of 6.9% in 2016, the DAX30 grew by 12.5% in 2017, more than the stoxx600 (+10.6%). But the index fell by 18.5% in 2018, which is a much lower performance than the Stoxx600NR (-10.7%). The DAX has posted a 9.5% increase since the beginning of the year, loosing momentum, compared with 12.1% for the Stoxx600 and 15.2% for the S&P500. The worsening of the trade war between the US and China is a significant risk for Germany, of which exports are heavily dependents of these markets.

Instruments : DBX (DB x-Tracker in Euro), DAXEX (iShares in Euro), DAX (Lyxor in Euro)