The ETF Lyxor AUT (UCITS), created in 08/2006 is listed on Euronext (Euro) and tracks the Stoxx600 Automotive index.

It allows the investor access to a basket of 17 major European stocks in the automotive sector, which are primarily German (58% of the capitalization).

The cost of this ETF is 0.3% in the middle of the range of our selection and the AUM is approximately € 43m. The replication method is indirect (via a swap) and dividends are capitalized.

Alternative ETFs: CARZ (First Trust, in USD)

Index & components

This index could almost be qualified as German because the first three stocks account for almost half of the index (Daimler: 257%, BMW 10% and Volkswagen 9%), while around a quarter of the index is composed of French stocks (Michelin, Peugeot, Renault, Valeo).

AUT is a rather narrow tracker which can be very volatile, because very cyclical, while deep transformations are in progress (electric car / autonomous car). The Chinese market is becoming the most important in the world and alliances are becoming an essential part of gaining market share.

The Volkswagen scandal on emissions - and the involvement of other manufacturers such as Renault and Fiat - are expected to deeply transform the market, which is likely to mean diesel deaths in the medium term and accelerating the transition to the hybrid and the all-electric a little later when batteries autonomy will allow it.

A new factor of complexity is the US administration, much more protectionist and that will not facilitate the task of European manufacturers. The intrinsically high volatility of this sector is expected to increase further in the future, while equipment manufacturers (Michelin, Continental and Valeo) represent a pole of growth and stability. Pressure on prices is high, but productivity gains are increasing and a number of manufacturers are doing well thanks to maintenance (spare parts, service). Another potential problem is the rise in interest rates, which if continued, could negatively impact sales of vehicles that are mostly carried on credit or leasing.

The current growth is mainly achieved in Europe and China, but in the longer term it seems to increasingly favor its domestic manufacturers and the electric car. The automotive sector is expected to remain volatile and face many shocks (technological in particular) in the future, while the electric car revolution accentuates the race to the critical size. Connectivity and the autonomous car will open the field to new disruptive industrial business models and new players like major technology companies could come to transform the industry in depth.

Latest developments

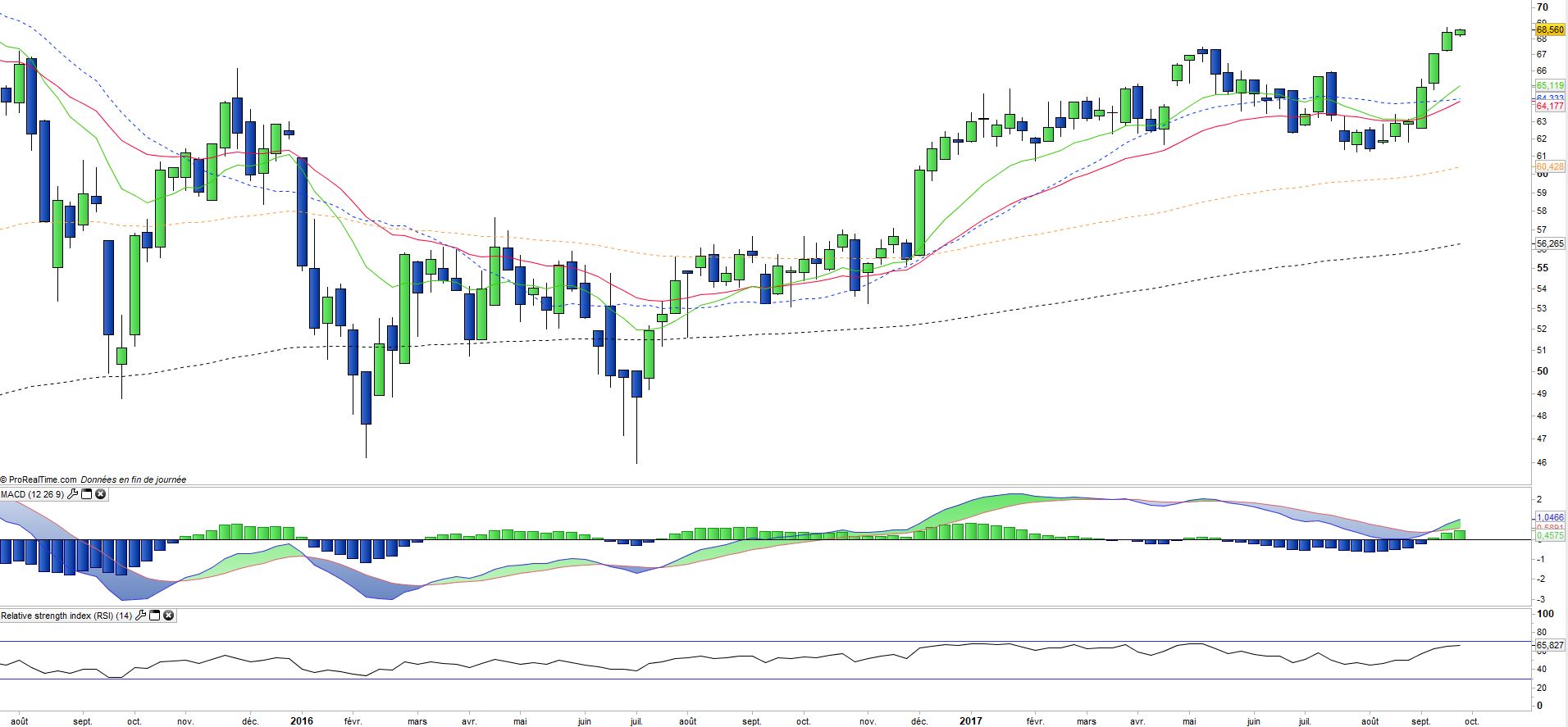

AUT increased by 11% since the beginning of the year, slightly more than the Stoxx600 (9%), which is mainly due to the strong growth recorded in September (+ 10.1%).

The sectors trend is positive for 2017, due to a very dynamic European market and exports expected to be held in emerging countries. In addition, the announcements on the electric car multiply (Daimler, BMW and Renault in particular) and the Frankfurt show has shown the very important ambitions of the manufacturers in this field.

On the other hand, the dynamic of profitable growth is confirmed and the valuation levels are at their lowest level since 2010. Consolidation is expected to continue after the acquisition of Mitsubishi by Renault and Opel by Peugeot, it would not be surprising that the next big move will come from China. The announcement this summer of a Brussels inquiry on a diesel cartel involving leading German manufacturers has chilled enthusiasm over the sector temporarily but the amount of possible fines is not yet known and remains purely speculative.