The ETF Lyxor BRE (Basic Resources UCITS Europe) created in 08/2006 is listed in Euro on Euronext and seeks to replicate the index STOXX600 Basic Resources Europe composed of 20 European stocks of which about 2/3 are English, which implies a significant risk related to the Euro – Sterling evolution which can be quite volatile in this period of Brexit. The costs of this ETF are 0.3% and the AUM of approximately 230M€. Replication is indirect (via Swap) and there is a dividend capitalization policy. This ETF is eligible for PEA.

Alternative ETFs: EXV6 (iShares in Euro)

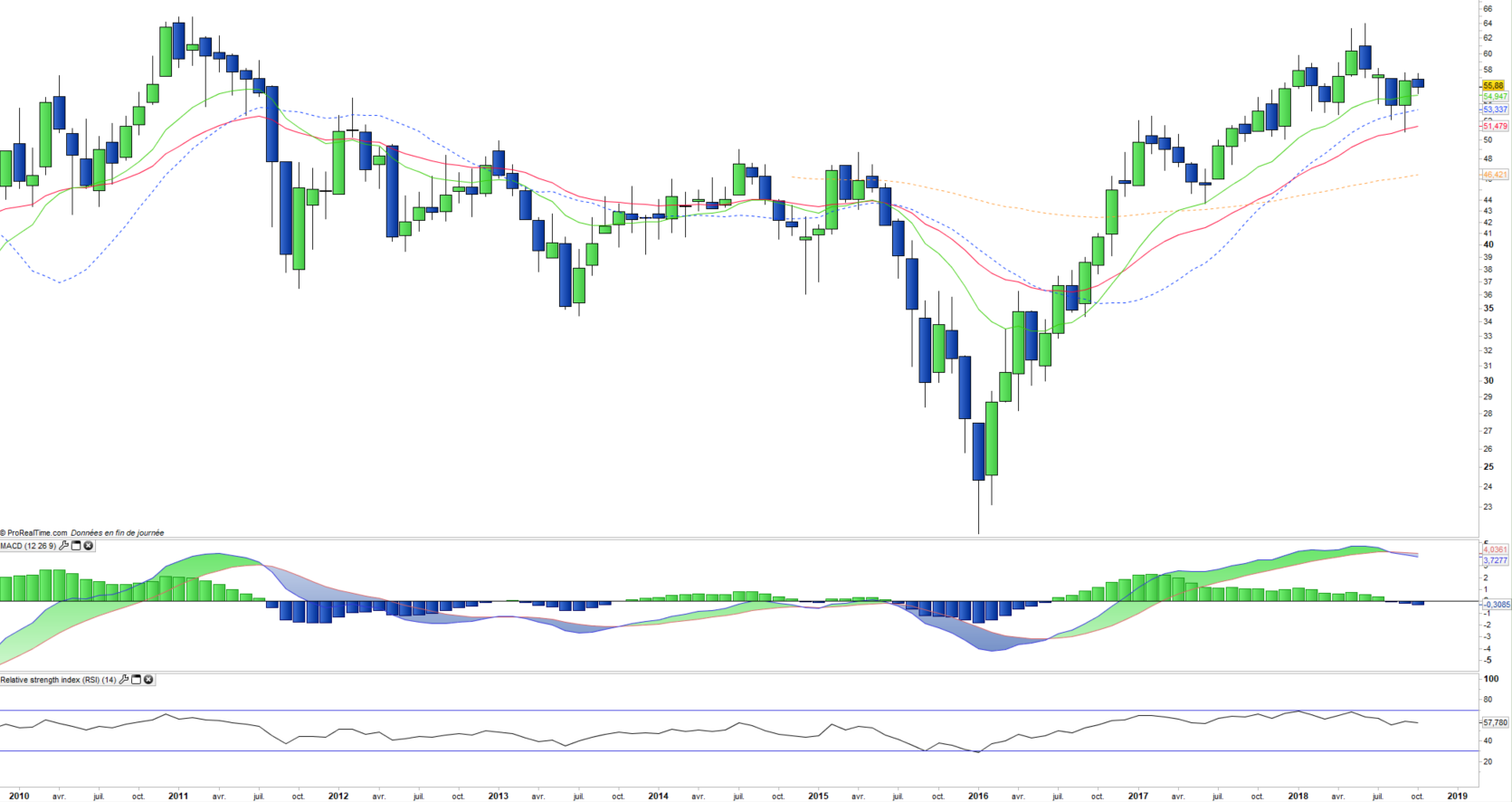

Latest developments

BRE was up 22.3% in 2017, well ahead of Stoxx600NR (10.6%), reflecting the rebound in commodities, which tended to stabilize in 2018.

Since the beginning of year, the index rose 0.2%, which is once again above the performance of stoxx600NR (-1.8%).

Commodity prices and the behavior of the mining sector remain highly correlated with China, the world's largest consumer, while the escalating trade war with the US is of growing concern to investors. After a fairly pronounced decline in most metals since June (copper, nickel ...), a stabilization is underway in anticipation of new fiscal stimulus measures and subsidies by the Chinese government to support the economy.

The strong world GDP growth, is likely to support the main end markets (construction, automobile, industry ...) and ultimately the commodity prices.

Index & components

This is a fairly narrow index composed of 20 major mining companies, mostly listed in the UK. The 3 largest mining companies, Rio Tinto, BHP Billington and Glencore account for c. 50% of the weighting of the index and are quoted in £ on the LSE. They are diversified mining companies (iron ore, copper, coal ...) with market capitalizations between € 50 and € 75bn. These companies are listed on European markets (especially London) but mining operations are most often located in Africa, Australia or the Americas.

After five difficult years (2011-2015), commodity prices started to recover in 2016, due to Chinese capacity reduction announcements (mainly steel and aluminum) and a surge of optimism around the world. Donald Trump's victory in the US presidential elections, tied to the promise of a major infrastructure program, as key triggers.

The prices evolution rather favorable in 2017 for a certain number of metals (aluminum, copper, Nickel, Palladium ...) because of a reduction of the overcapacities coming from China, and growth themes like the electric car and renewable energies. The current demand is also largely due to China's monetary support for its economy (real estate / construction in particular) and can therefore seem a bit fragile. Diversification is at the heart of the strategy of the major mining companies who wish rather to develop capacities in the sectors of the future (Aluminum, Copper ...) and to reduce them in troubled sectors (Coal ...).

The sector depends on two main factors, namely demand, especially for infrastructure and the industrial sector (construction and automotive), mainly from China and the US, but also from Europe and major emerging countries such as India, but especially of the supply side so far plethoric.

The scenario of a drastic decline in Chinese capacity does not seem to be on the agenda, especially in iron ore, but the introduction of the US import tax on certain metals (aluminum) could incite China to more discipline on its supply policy.

BRE remains a rather volatile medium, which is very sensitive to variations in demand but also to supply adjustments.