Amundi ETF China (CC1) - 08/11/2018

Short Term strategy: Positive (70%) / Trend +

Long Term strategy: Positive (60%) / Trend +

Characteristics of the ETF

The CC1 ETF (Amundi) created in 03/2009 is listed in EURO on Euronext and replicates the MSCI China-H net dividends reinvested index ("net return"), which is composed of the main Chinese stocks listed in Hong Kong and composed for 2/3 of financial values. These shares are subject to Chinese regulation but denominated in Hong Kong dollar (HKD). Chinese H shares, unlike A shares, are available to non-resident investors in China. The target for maximum tracking error between changes in the net asset value of the Fund and that of the MSCI China H Index is 2%. This tracker presents a currency risk linked to the exposure of the MSCI China H Index, resulting from the evolution of the reference currency, the Hong Kong dollar (HKD).

The fee of this ETF is 0.55% for an AUM of 153M €. The replication method is synthetic (via swaps).

Alternative ETFs: CSIA (Lyxor in Euro), FXI (iShares in USD)

Latest developments

After a rise of 13.6% in 2017, CC1 is down -3.4% in 2018, which is mainly related to the credit restrictions decided by the Chinese authorities as well as the US-China trade war, which led to a rise in tariffs on $ 250 billion of Chinese exports to the USA.

Chinese statistics have recently shown signs of weakness in investment while consumption remains dynamic. However more positive news could come in the coming weeks, with the Chinese authorities likely to boost the economy to support the economy, while negotiations between the US and China are not excluded now that the mid-term elections have passed.

The sharp decline in the Chinese index, which is linked both to the international context and the decline in the currency seems to take into account many negative developments.

Index & components

The equities that make up the MSCI China-H Index come from the universe of the most important stocks in the Chinese market.

The MSCI China-H Index is composed of 68 constituents, so it is relatively diversified. The financial sector (banks and insurance companies), however, accounts for about 68% of the capitalization while the China Construction Bank accounts for 16% of the index.

China is the world's second largest economy behind the US with a GDP of about $ 13600bn in 2017, the world's largest exporter with the world's largest foreign exchange reserves.

The global recession of 2009 interrupted China's continued growth momentum, and the limits of its export-oriented growth model emerged. As a result of the global economic downturn and declining trade, Chinese growth decelerated to below 7% in 2015, its lowest level in 25 years. However, in 2017, growth reached 6.9% of GDP, an improvement over 2016 (6.7%). State-owned enterprise debt accounts for 145% of GDP while private sector debt accounts for more than 200% of GDP. In addition, the quality of bank assets has deteriorated for several years and this trend is probably underestimated because of the importance of the shadow banking.

Many challenges remain linked to the problem of an aging population, the lack of openness of the political system, the competitiveness of an economy dependent on high investment expenditure and the expansion of credit. The manufacturing and construction sectors contribute nearly half of China's GDP, but the country is increasingly relying on services and domestic consumption.

China has set a new growth target for 2018 of around 6.5%, which means a gradual soft landing linked to the new growth model, more based on quality, corresponding to an upscaling of industry and services, but also focused on reducing the current major imbalances (too high debt, overcapacity in industry and real estate).

China no longer seems to be in the race for growth, but in search of a more balanced and sustainable model based on the upscaling of its industry through technology and the expansion of services and domestic consumption.

China faces geopolitical problems with most of its neighbors (India, Japan ...) and especially in the China Sea, because of its plans for territorial expansion that could lead to military confrontations. Its confrontation with the USA, at the commercial level, could be amplified under the background of the Korean crisis.

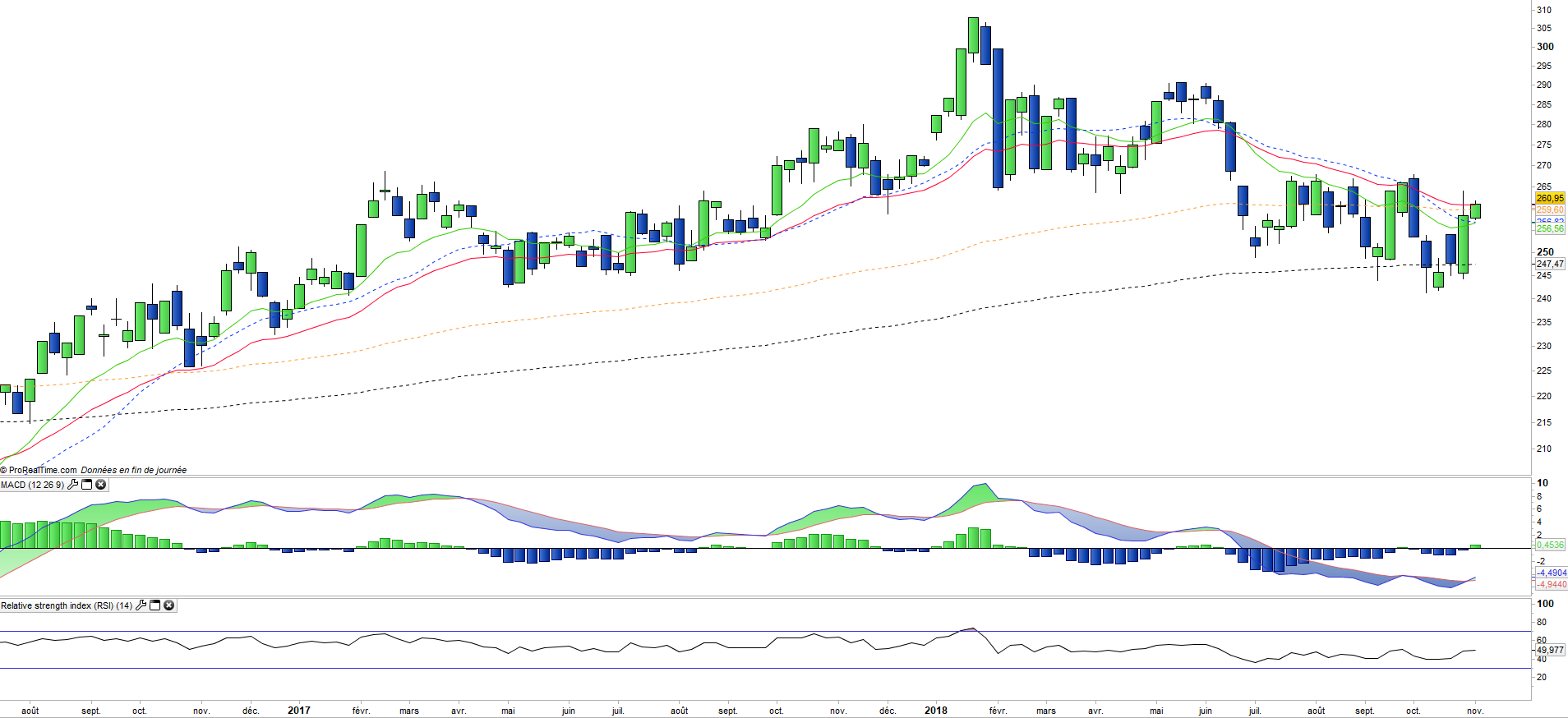

Monthly data

The analysis of the monthly charts shows a trend that has not completely returned despite the strong consolidation that has been raging since the beginning of the year. Some stabilization is underway, which is visible at the level of moving averages and oscillators. The MACD remains above its zero line and the RSI still meets the 50 level. A recovery remains possible while the decline loses momentum.

Weekly data

Weekly chart analysis shows a credible bullish attack that is spilling over both the EMA26 and the EMA100. This attack is credited by the bullish reversal of the MACD accompanied by other technical oscillators. A reversal of trend is underway over the medium term horizon with the objective of the level of € 285 which corresponds to the bearish departure of the beginning of summer.

ETF Objective

CC1 is a UCITS ETF, listed in EUR, which seeks to replicate the MSCI China H index (68 chinese companies)

Characteristics

| Inception date | 03/03/2009 |

| Expense ratio | 0,55% |

| Issuer | Amundi |

| Benchmark |

MSCI China H

|

| Code/Ticker | CC1 |

| ISIN | FR0010713784 |

| UCITS | Yes |

| Currency | Euro |

| Exchange | Euronext Paris |

| Assets Under Management | 153 M€ |

| PEA (France) | Yes |

| SRD (France) | Yes |

| Currency Risk | Yes |

| Number of Holdings | 68 |

| Risk | 4/5 |

Country breakdown

| China | 100% |

Sector Breakdown

| Financials | 66% |

| Energy | 10% |

| Industrials | 7% |

| Materials | 4% |

| Consumer discretionary | 3% |

| Utilities | 2% |

| Health Care | 2% |

| Others | 5% |

Top Ten Holdings

| China Construct Bank | 16% |

| ICBC | 10% |

| Ping an Assurance | 10% |

| Bank of China | 7% |

| China Petroleum Chem | 5% |

| Petrochina Co | 3% |

| China Life Insurance | 3% |

| Agricult BK China | 3% |

| China Merchants Bk | 3% |

| China Pacific Insur | 2% |