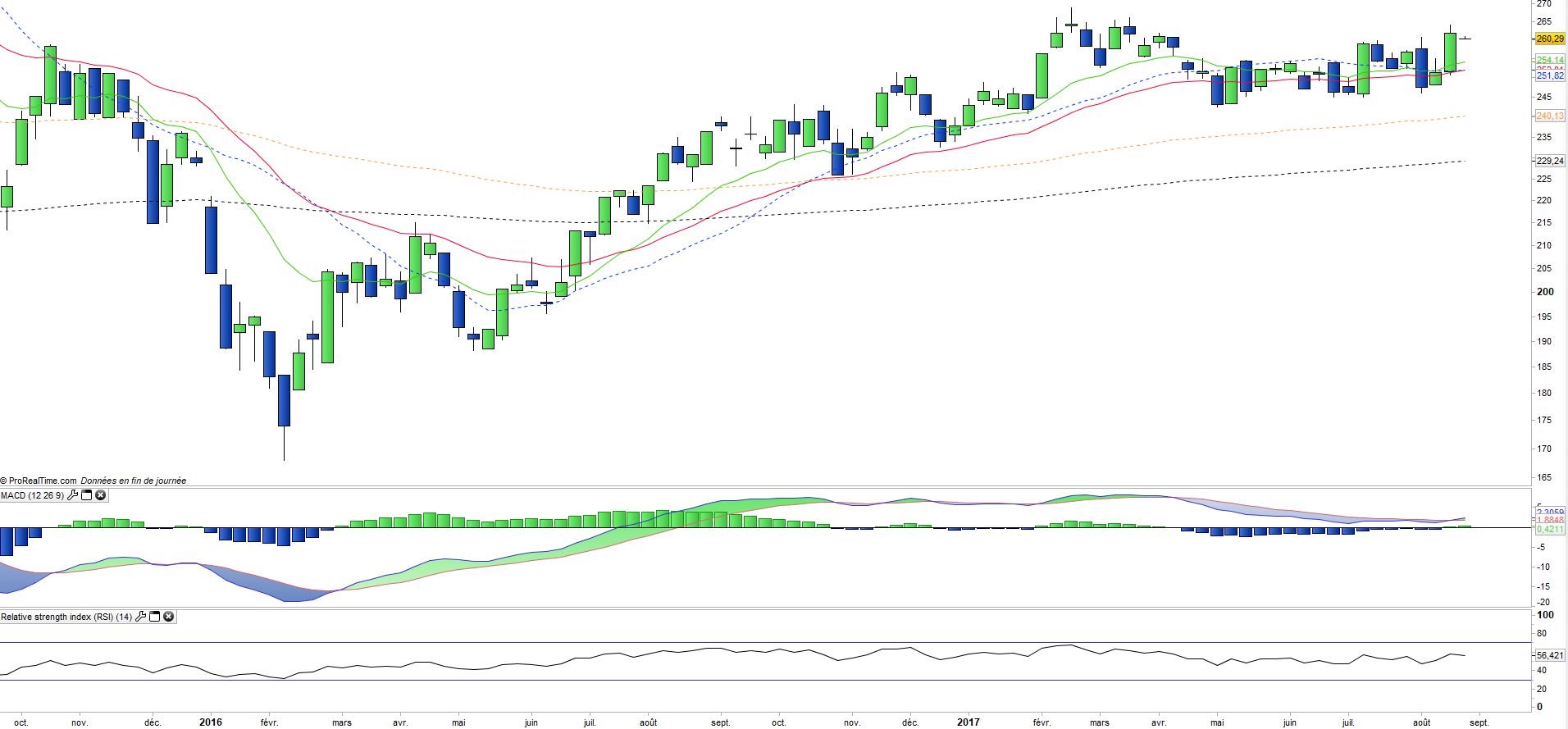

ETF CC1 (Amundi) replicates the MSCI China H index, dividends reinvested (net return).

The shares included in the MSCI China H Index are derived from the world's largest value universe in the Chinese market. The MSCI China H Index is composed of 69 constituents and is therefore relatively diversified. The financial sector (banks and insurance companies), however, accounts for two-thirds of the capitalization while China Construction Bank accounts for 15% of the index.

Chinese equities H are the shares of mainland China (Hong Kong) listed companies or other foreign exchanges. These shares are subject to Chinese regulation but denominated in Hong Kong dollar (HKD). H shares are, unlike A shares, available to non-resident investors in China. The maximum tracking error between the Fund's NAV and the MSCI China H Index is 2%. This tracker has a currency risk related to the exposure of the MSCI China H Index, resulting from the change in the reference currency, the Hong Kong dollar (HKD). Dividends are capitalized and the cost of this ETF is 0.55%, which is fairly typical for an emerging index. This ETF makes it possible to hold the main Chinese companies in the portfolio.

China is the world's second largest economic power behind the US with a GDP of around $ 12,000 billion in 2016, the world's largest exporter and the world's largest foreign exchange reserves. The global recession of 2009 interrupted the continuous growth momentum in which China was engaged, and the limits of a growth focusing on exports were most evident. Given the global economic downturn and falling trade, China's growth has decelerated to below 7% in 2015, its lowest level in 25 years, and this trend continues. In 2016, growth reached 6.6% GDP. The debt of state-owned enterprises accounts for 145% of GDP, while private sector debt would have accounted for nearly 210% of GDP in March 2016.

Consumption is slowing and the yuan's decline against the dollar currently leads to capital flight, as a result the central bank's foreign exchange reserves are dwindling. Moreover, the quality of banking assets is deteriorating and this trend is probably underestimated due to the importance of shadow banking. There are still many challenges related to the problem of an aging population, the shrinking of the labor force, the lack of openness of the political system, the competitiveness of an economy dependent on high investment spending and credit. Manufacturing and construction sectors contribute nearly half of China's GDP, but the country is increasingly focusing on services and domestic consumption.

China has just set its new growth target for 2017, at around 6.5% (which is currently slightly above expectations), so a gradual soft landing linked to the new growth model, based more on quality that corresponds to an upgrading of the industry and services but also focused on reducing the current major imbalances (excessive debt, overcapacity in industry and real estate). China no longer seems to be in the race for growth, but in search of a more balanced and sustainable model whose base is the rise of its industry through technology and the expansion of services and domestic consumption.

China faces geopolitical problems with most of its neighbors (India, Japan ...) and especially in the China Sea, because of its plans for territorial expansion which could lead to military confrontations. But as we have just seen with the Bhutan crisis with India, China remains rational and cautious. Its confrontation with the US, which has just triggered an investigation into its business practices, could be amplified under a crisis of Korean.