Lyxor FTSE ATHEX Large Cap (GRE) - 20/12/2017

Short Term strategy : Positive (70%) / Trend +

Long Term strategy : Positive (45%) / Trend -

Characteristics of the ETF

The ETF GRE (Lyxor) created in 01/2007 is quoted in Euro on Euronext and replicates the index FTSE ATHEX LARGE Net Total Return CAP composed of the 25 largest companies listed on the Athens Exchange (ATHEX).

The fee of this ETF is 0.45% for AUM of € 185m. The replication method is indirect (via swap) and there is an annual dividend distribution policy.

Alternative ETFs: GREK (Global X in USD),

Index & components

The ETF GRE is composed of 25 companies, so it is rather narrow compared to the other national indices but finally quite diversified with 27% for the financial sector which gathers the main banks of the country (Alpha Bank, National Bank of Greece, Eurobank ergasias , Piraeus Bank), the consumer goods sector accounts for 22% (mainly the Coca-Cola subsidiary), 11% for telecoms (Hellenic Telecoms), while the remaining part of the index is mainly the industrial sector (Cement, energy, materials), to note the presence of a gaming company / paris: OPAP, which represents nearly 9% of the capitalization.

The Greek economy is roughly at the level of Portugal, with a GDP of about € 200 billion. The worst seems to have passed for Greece, which returned to growth in 2016 at + 0.3% and the European Commission expects + 1.6% in 2017 and + 2.5% in 2018. Thanks to the economic diversification led by the country, the industry replaced agriculture as the second largest source of income after services, accounting for 15.7% of GDP and employing 15% of the labor force, although its share was larger (20%) before the financial crisis. The main sectors are electronics, transportation equipment, clothing and construction. Greece has the largest maritime fleet in the world and the tertiary sector accounts for 80% of GDP and employs 71% of the active population while tourism alone contributes 11% of GDP. Greece has an outward-oriented economy, with trade accounting for 64% of GDP, and Greece's main trading partners are the European Union (especially Italy and Germany), Turkey and Russia.

In 2016, the budget deficit decreased thanks to a VAT reform and a better tax collection, nevertheless, bank deposits remain low and the control of capital continued in 2016, as a result, business transactions with foreigners remain constrained. Capital controls also affected exports related to shipping. If progress continues, Greece could benefit from significant debt relief, depending of the next German coalition. This recovery is due to renewed confidence in improving relations between the government and the international financial community. Greece has successfully returned to the markets, placing a five-year bond for the first time in three years, the Greek state borrowed 3 billion euros at a rate of 4.625%, lower than that obtained during the last bond issue, in 2014, which was 4.95%. This was confirmed in November by a second bond swap transaction for an amount of € 25.5bn.

This is encouraging and shows the progress made. Economic activity recovered in 2017 thanks to the banking sector, which continues to stabilize, and a more favorable European context. The rating agencies upgrade their rating one after the other. After a lost decade, Greece seems to be able to gradually regain its financial and budgetary autonomy.

Latest developments

GRE grew by 18.9% in 2017, following a stabilization in 2016 (-0.9%). Greece is expected to exceed its budget surplus target in 2018 for the third year in a row, which could help ease its austerity policy. In the latest budget projection, the government is counting on a primary surplus - that is, out-of-service debt - between 2.4% and 2.5% this year and over 3.7% in 2018. these figures are higher than previous forecasts.

A strong primary fiscal surplus could enable the government, which is coping with the population's weariness in the face of tax increases and declining pensions, to redistribute some resources to the poorest. The country has just emerged from several years of recession, which has erased about a quarter of its GDP and boosted the unemployment rate to nearly 28%. The unemployment rate in Greece continued its decline in the third quarter of 2017, standing at 20.2% against 22.6% a year earlier, even if it remains the highest in the euro zone. A possible German coalition with the SPD would be much more favorable to Greece than a coalition with the Liberals that exclude any renegotiation of the debt and any transfer of wealth to the most vulnerable countries.

The Greek banking system is strengthening, and growth looks set to accelerate upwards in 2018, with a forecast of around 2.5%.

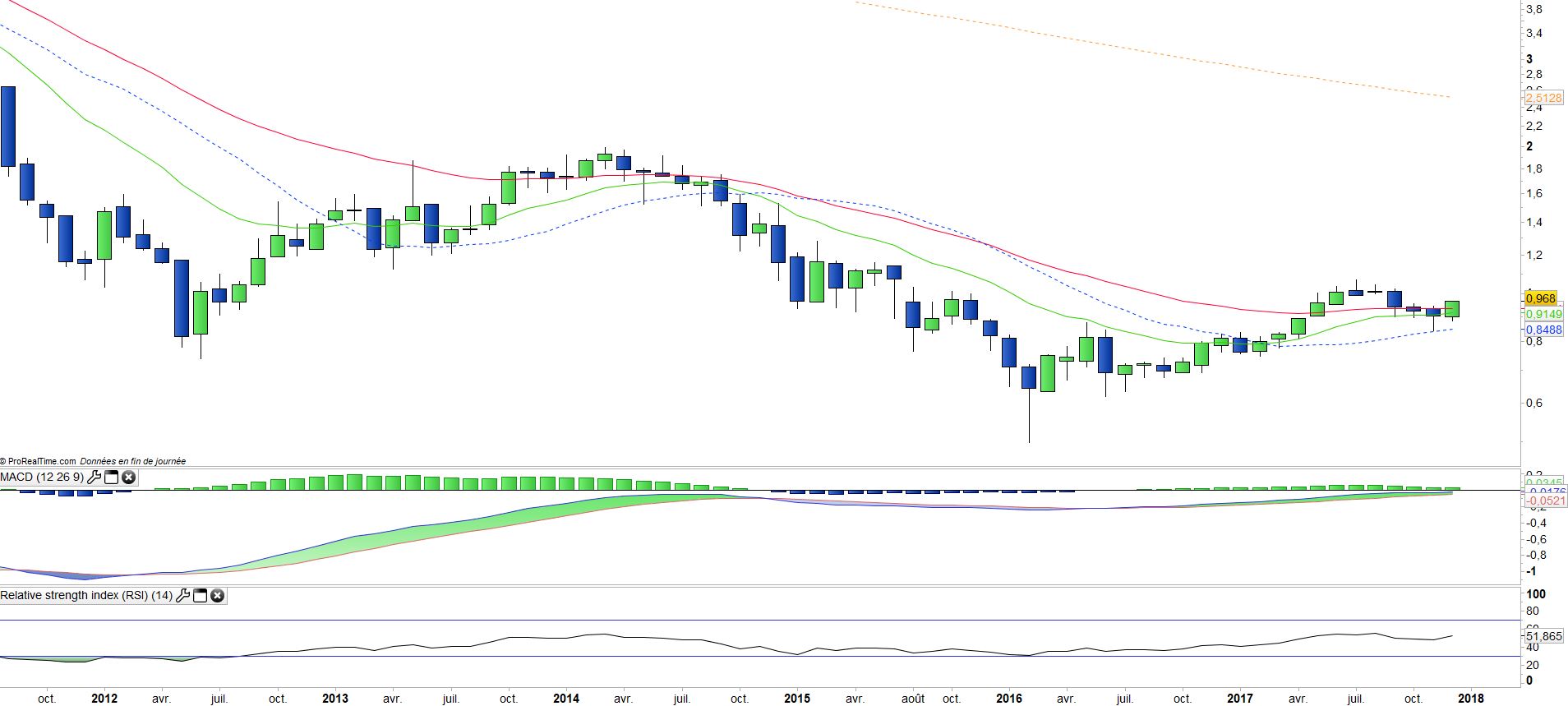

Monthly data

The monthly chart shows a long-term bearish trend that is coming to an end. After a first overflow and a rebound on the EMA100, GRE starts a new surge above EMA13 and EMA26, which must be confirmed at the end of the month.

The MACD is moving towards its zero line, which could be crossed soon. The technical configuration is encouraging and suggests a reversal with high potential.

Weekly data

On the weekly chart, we can see that the reversal is being confirmed. Prices are standing above the 13x26 moving averages, which are close to crossing as well as the MACD. It does not miss much to validate a medium-term bullish signal, but it is as always preferable not to anticipate and wait for the realization of these technical signals.

If prices manage to remain above moving average until the end of December, there is a good chance that the trend reversal will be confirmed.

ETF Objective

GRE is a UCITS ETF which seeks to replicate the benchmark index FTSE ATHEX LARGE CAP Net Total Return (25 companies)

Characteristics

| Inception date | 05/01/2007 |

| Expense ratio | 0,45% |

| Issuer | Lyxor |

| Benchmark | FTSE ATHEX Large Cap |

| Code / Ticker | GRE |

| ISIN | FR0010405431 |

| UCITS | Yes |

| EU-SD status | Out of scope |

| Currency | € |

| Exchange | Euronext Paris |

| Assets Under Management | 189 M€ |

| Replication Method | Indirect (swap) |

| PEA (France) | Yes |

| SRD (France) | Yes |

| Dividend | Capitalization |

| Currency Risk | Yes |

| Number of Holdings | 25 |

| Global Risk | 4/5 |

Country Breakdown

| Greece | 78% |

| Switzerland | 21% |

| Belgium | 1% |

Sector Breakdown

| Financials | 27% |

| Consumer Staples | 22% |

| Consumer Discretionary | 17% |

| Telecom Services | 11% |

| Industrials | 6% |

| Energy | 6% |

| Materials | 5% |

| Others | 6% |

Top Ten Holdings

| Coca Cola HBC | 21% |

| Alpha Bank | 11% |

| Hellenic Telecom | 10% |

| OPAP | 8% |

| National Bank of Greece | 7% |

| Eurobank Ergasias | 6% |

| Jumbo SA | 6% |

| Motor Oil | 4% |

| Mitilineos Holdings | 4% |

| Titan Cement | 4% |