The JPN ETF (Lyxor UCITS) created in 08/2006 is listed in euros on Euronext and replicates Topix Gross Total Return index which is composed of 2080 Japanese stocks, while each share is weighted according to its market capitalization. This index embeds a risk related to the evolution of the Euro / Yen pair linked to the economy and the policy of the central banks of the two zones.

The fee of this ETF is 0.45% for an AUM of € 1 548M. The replication method is direct (physical) and there is a policy of semi-annual distribution of dividends.

Alternative ETFs: TPXH (Amundi in Euro), EWJ (iShares in USD), EJAH (BNP Easy in Euro)

Index & components

The Topix index is of a very great depth and the most representative of the Japanese economy.

The industry in all its forms (consumer goods, equipment, heavy industry ...) is strongly represented in the index (overall around 50%) with a financial sector that weighs 11.9% and a health sector to 6.9% while the technology sector is fairly large and accounts for 12.3% of the index. In the first 10 capitalizations, which represent about 16% of the Topix index, we will find automakers (Toyota, Honda), and groups such as Mitsubishi, Softbank and Sony as well as financials.

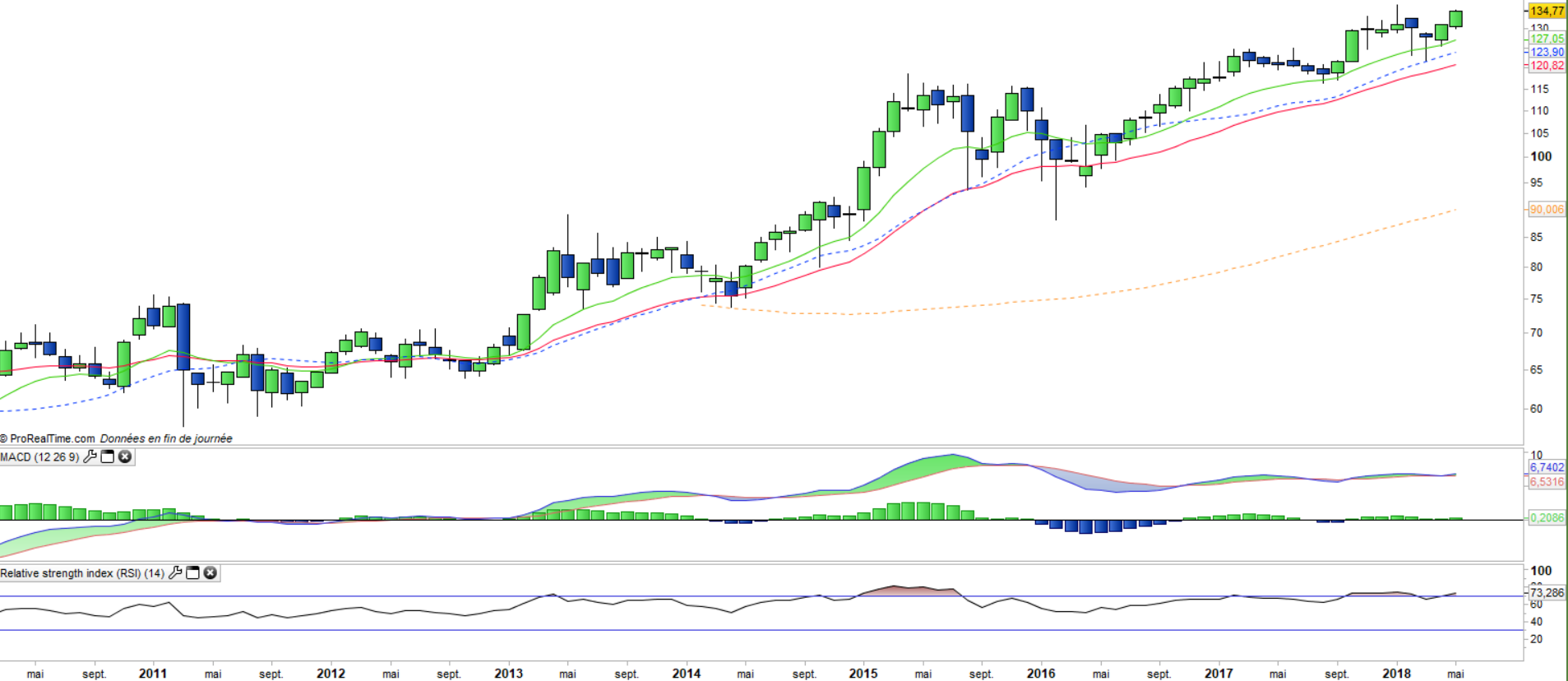

The cumulative performance of this ETF since January 2010 is around 113%, which also includes Yen / Euro currency movements (Topix performance over the period reach 127%).

The Japanese economy is the world's third largest, behind the US and China, with a GDP of about $ 5000 billion, it is a very diversified economy based on services and industry / advanced technology and whose model of growth is based on exports of consumer goods (automotive, technological goods) of capital goods and infrastructure, which is somewhat similar to that of Germany.

The Japanese economy is quite dependent on the evolution of its currency with the main world currencies (Dollar, Euro, Renminbi, Sterling), while the most important problem remains that of the deflation which lasts for two decades. This deflation first came from a time adjustment of the price of assets that had entered a bubble (1980s), but it is also due to a structural problem linked to the declining demography not offset by immigration.

Japan is today the most indebted country in the developed world but the national debt is held by the Japanese and not by foreign funds which limits the risk of financial crisis, but which, on the other hand, forces the economic recovery. The reassuring news from China and the deepening of the economic partnership with India, however, are favorable factors while the current valuation of the Japanese index remains reasonable with a potential for high earnings growth.

Latest developments

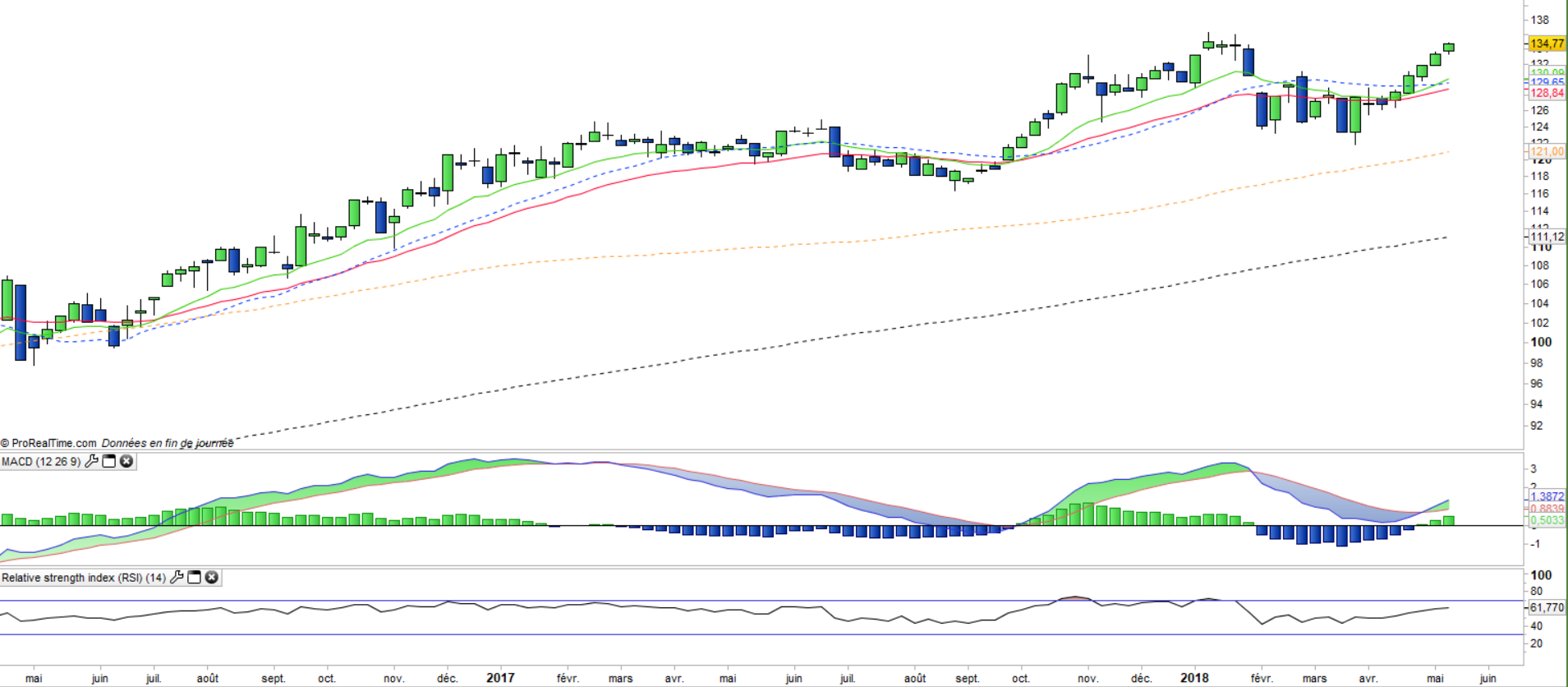

After a rise of 6.6% in 2016, the performance of JPN accelerated in 2017 to + 10.7%.

The index has risen 3.9% since the beginning of the year despite the correction coming from the US and has impacted most of the world's places. Despite a contraction in GDP in Q118, global demand remains strong, especially from the United States, and Japanese exporters should quickly take advantage of large orders, especially in computing for cloud solutions. Over the year as a whole, GDP growth should however be less dynamic than last year.

Trade tensions between China and the United States continue to weigh on the confidence of the country's major companies, which are highly dependent on these two major markets. However, the positive developments of the WE (agreement between the US and China on the reduction of Chinese surpluses) should be welcomed. In addition, valuations of the index remain reasonable at around 16x earnings at 12 months for earnings growth expected between 7 and 10%.

The main element to watch is the evolution of the YEN / USD parity, which has tended to stabilize in recent months, but which could end up affecting the competitiveness of Japanese companies in the event of a sharp rise.