The ETF L100 (Lyxor) created in 04/2007 which is listed in Euro on Euronext, replicates the FTSE100 index which is composed of the 100 main English stocks representative of the main sectors of the UK economy, while the holdings are selected according to the importance their float-adjusted market capitalization. No component can represent more than 15% of the index.

The ETF's fees are quite low at 0.15% and the AUM is around € 522M. Replication is indirect (via swap) and there is a dividend capitalization policy.

Alternative ETFs: ISF (iShares in GBP), VUKE (Vangard, in GBP), C1U (Amundi in Euro)

Index & components

The ETF L100 (Lyxor) is quite deep, and above all fairly balanced from a sectoral point of view. Nevertheless, we note the particularity of a significant weighting in the commodities sector, since all the oil & gas + mining sectors represent 25.4% of the index (versus 6% for the stoxx600), more than the financial ones (21.4%) and consumer durables (17.3%). The health sector is also very important and accounts for 9% of the index.

All this implies that the FTSE 100 is very "dollarized" because these companies revenues are usually largely made in the US currency, which is not trivial either given the potential amplitude of the change in the USD/EURO. The FTSE 100 is of course quoted in pounds, so there is a particular exposure to the UK currency on the L100 ETF which is quoted in euros, and has naturally decorrelated from the FTSE100 index for some time for these reasons.

If the "Brexit" has not turned into financial stress or stock market panic, it must be said that the shock transmission belt was the British currency which has fallen about 20% against both the Euro and the USD. The effective exit of the UK, 6th world economy is expected to occur in the first half of 2019, while the triggering of Article 5 was realized as planned in March 2017, its effects should be felt in the long run as it will probably require an adaptation of the English model. An extension of the period of talks (with status quo preservation) for another 2 years is quite likely especially if the negotiations move towards an agreement, a hypothesis that does not seem to be excluded. Europe is for the moment united in front of England, and remains firm on its demands, while threats of dislocation of the United Kingdom are not very far apart (reunification of Ireland under the European flag and the Scottish referendum).

On the other hand, the good short-term news of the fall in the pound for UK exporters has now negative impacts, such as inflation and rising interest rates, which should continue according to the BOE.

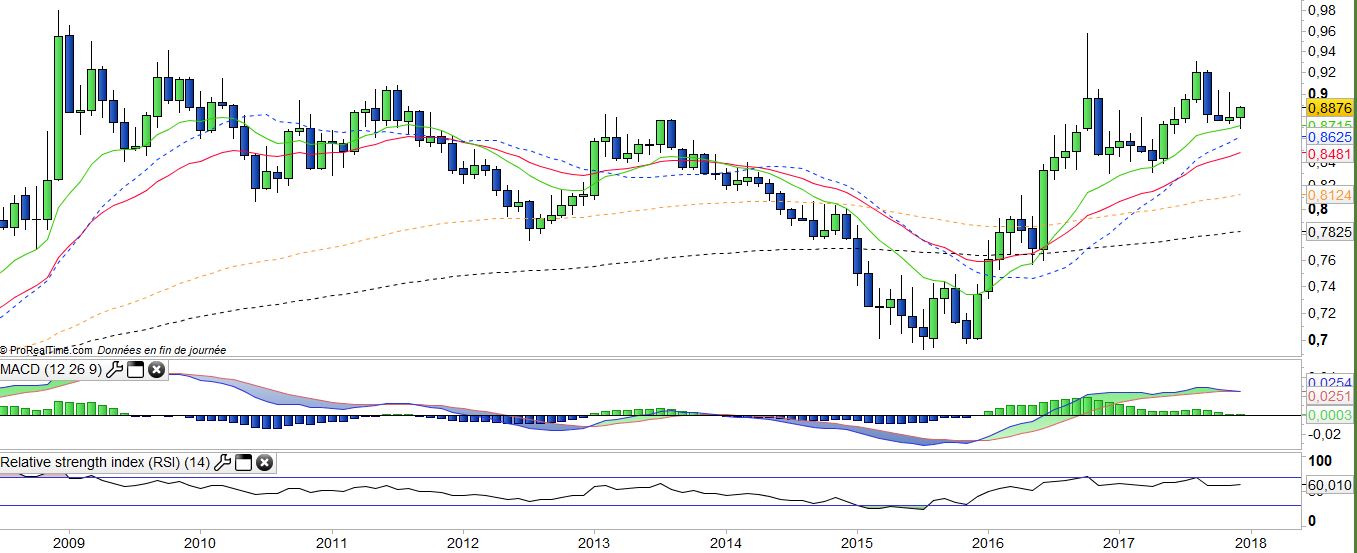

Latest developments

The English index shows a + 6.6% increase since the beginning of the year, a little behind the Eurostoxx50 performance (+ 8%), but which includes a significant catch-up in December (+3.6% for the FTSE100 against -0.5% for the Eurostoxx50) thanks to the good performance of the oil and mining sector.

The Brexit is beginning to be felt on the British economy, the IMF estimates that for the whole year, the growth of the GDP would reach 1.6%, less than in the two previous years, before slowing down slightly to + 1.5% in 2018 due to lower growth in household spending, which has tended to weaken in recent quarters due to the return of inflation and the fall in the GBP, as well as investments also in moderate growth. These figures are significantly lower than the ECB's anticipated annual growth for the Euro area, at 2.2% for 2017 and 2.1% for 2018.

The Bank of England (BoE) has begun a new cycle of rising interest rates in November (25 bp) raising its key rate to 0.50% while inflation has reached 3% above the 2% target, further increases are expected in 2018. At the political level, the Great Britain and the EU reached a first agreement on the terms of their divorce, to be held in March 2019, paving the way for negotiations over a transitional period after that date and on a future trade agreement that will govern subsequently relations between the United Kingdom and the EU.