The ETF MIB (Lyxor FTSE MIB40) created in 11/2003, listed in Euro on Euronext, replicates the Italian national index, composed of the 40 main Italian securities. The composition of the index is determined on the basis of three criteria: free float, liquidity and the representativeness of the main sectors of the Italian market.

The ETF MIB charges are 0.35%, and the AUM is approximately € 630M. Replication is indirect (via swap) and there is a dividend distribution policy.

Alternative ETFS: EWI (iShares USD), IMIB (iShares in Euro)

Index & components

This index has the particularity of being very overweight in financials which represent more than one third (38.7%) of its composition (against about 20% for the stoxx600), including Intesa San Paolo, Unicredit and Generali while the energy is also a significant weight (14.6%) via ENI and Saipem. The other important sectors are cyclical consumer goods (15.3%) and utilities (13.7%), among which are Enel , SNAM and Atlantia.

The 10 largest caps represent just over two-thirds of the index.

The Italian index is very volatile, given the importance of cyclical and financial sectors and the structural weakness of the Italian economy due to lack of growth, high unemployment and huge debt (134% of GDP) which worries the markets regularly. The Italian economy has been hit hard by the financial crisis: it has contracted by more than 9% since 2007 and has faced 13 quarters of recession. Although the Italian economy has emerged from the recession since 2015, growth remains below the Italian government expectations and the euro area average. In 2016 the country was hit by two earthquakes and the arrival of 170,000 migrants on its territory which led to a major humanitarian crisis. Italy made good progress in its banking restructuring in 2017 with the rescue of state-owned banks and the takeover of assets by Intesa Sanpaolo, which followed the rescue of BMPS, as well as the refinancing of Unicredit for 13bn€ in the first quarter of 2017.

Overall, the structural factors (banking system reforms and labor flexibility) are taking shape, and the business cycle is accelerating. The Euro / USD exchange rate remains a significant factor for the Italian economy driven by exports.

Latest developments

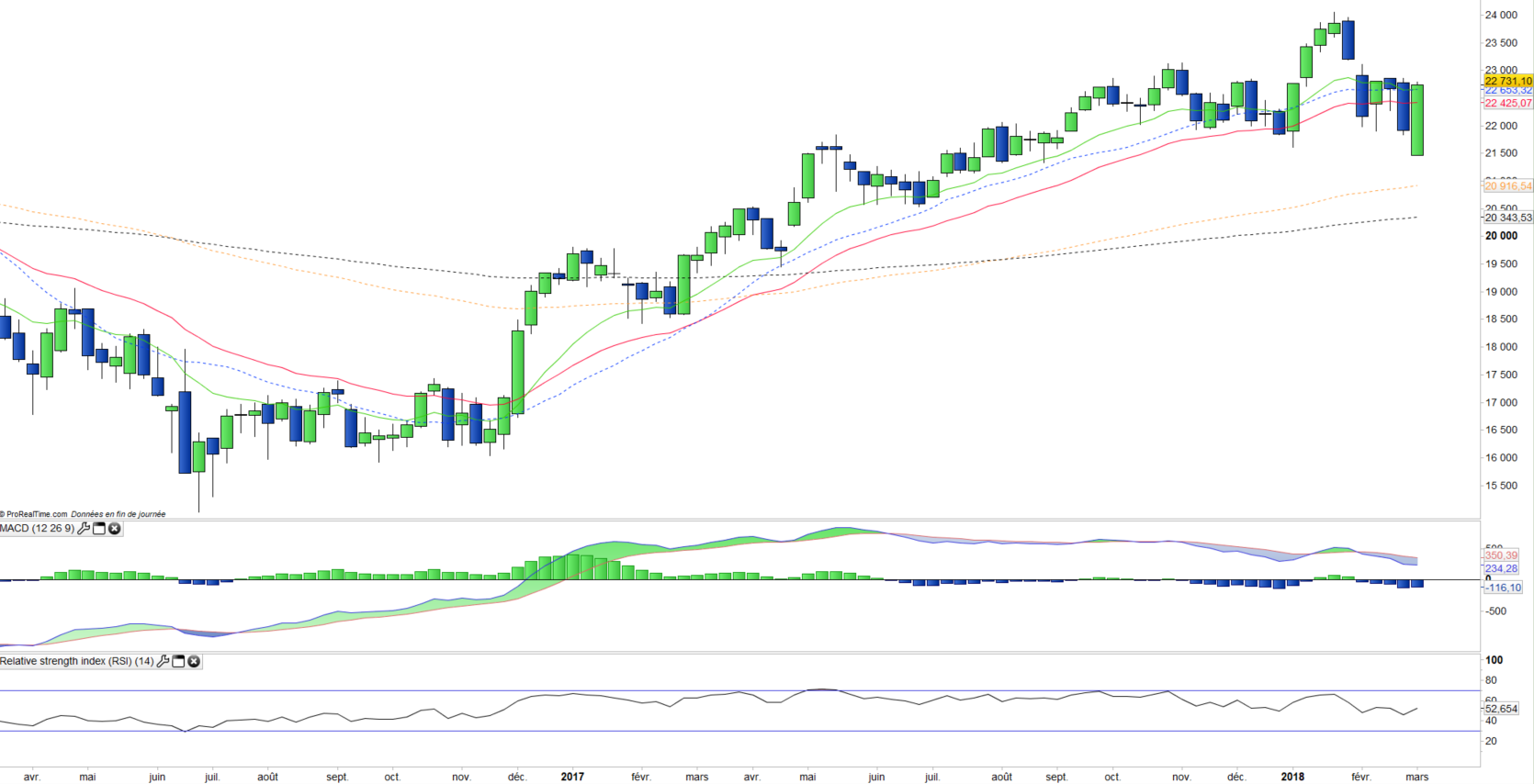

In 2017, the index posted an increase of 13.6% (against 10.6% for the stoxx600NR) and rose by 4% in 2018 supported mainly by banks (+ 9.8% for ISP and + 10.4% for Unicredit). Although improving (GDP: + 1.4% in 2017), Italian growth remains below the European average (+ 2.5%), which is due to high debt (134% of GDP) and unemployment which remains at a high level around 11%.

The elections of March 4 lead as expected to a stalemate: the right-wing coalition comes first, with 37% of the vote which will give 252 seats, the center-left coalition gets 23% of the vote, or 107 seats, the left is at 3%, 8 seats. But the real winner is the Five Star Movement, totally unclassifiable and antipolitic, which gets 32% of the vote and can count on a parliamentary group of 235 deputies. Italy should remain ungovernable and new elections are likely within 12 to 18 months, which does not seem to worry too much the markets after the same scenario has occurred in Belgium, then in Spain and even in Germany which has it took almost six months to form a coalition.