The SPY ETF (SPDR) created in 01/1993 replicates the S & P 500 index, which is composed of the 500 main US stocks representative of the main sectors, while the stocks are selected according to the size of their market capitalization.

The ETF fees are quite low at 0.0945% and the AUM is $ 264bn. Replication is direct (physical) and there is a dividend distribution policy on a quarterly basis.

Alternative ETFs: AUM5 (Amundi in Euro), SP5 (Lyxor in Euro), IVV (iShares, in USD)

Index & components

The top 10 stocks of the S & P500 include five major technology stocks (Apple, Amazon, Microsoft, Alphabet and Facebook), but also larger, more classic and iconic American companies such as JP Morgan or Exxon Mobil.

The main advantage of this index is its depth, which allows it to be a good proxy for the US economy, with a sector weighting that favors the growth sectors a little more, just like the technology stocks that represent about 24% of the weighting. Financials account for just under 15% of the index, and energy values of 6% are well balanced by defensive sectors such as health (about 14%) and consumer discretionary (13%).

The index has benefited from a strong momentum since the election of D. Trump, more than a year ago, while alongside the technology that remains the engine of the US market, new sectors have joined the trend, however a correction is now underway on the index because of fears of a return of inflation following the program of lower taxes for US businesses and households that should have a positive impact on growth, while announced deregulation on shale oil and banks could also benefit these sectors.

However the multiples of the S & P 500 are currently quite high, even after the ongoing correction at around 18x the results at 12 months, which is at the top of range (historically between 15 and 20x) even if it must be put in American economy growth estimated at around 3% in 2018. The whole question is now about the duration of the US cycle in a context of rising rates which is still progressive for the moment while the level of margins companies is at its highest level and seems to have lost much upside potential, even though the consensus is again on double-digit earnings growth in 2018 driven by the energy / oil sector, banks and technological values.

Latest developments

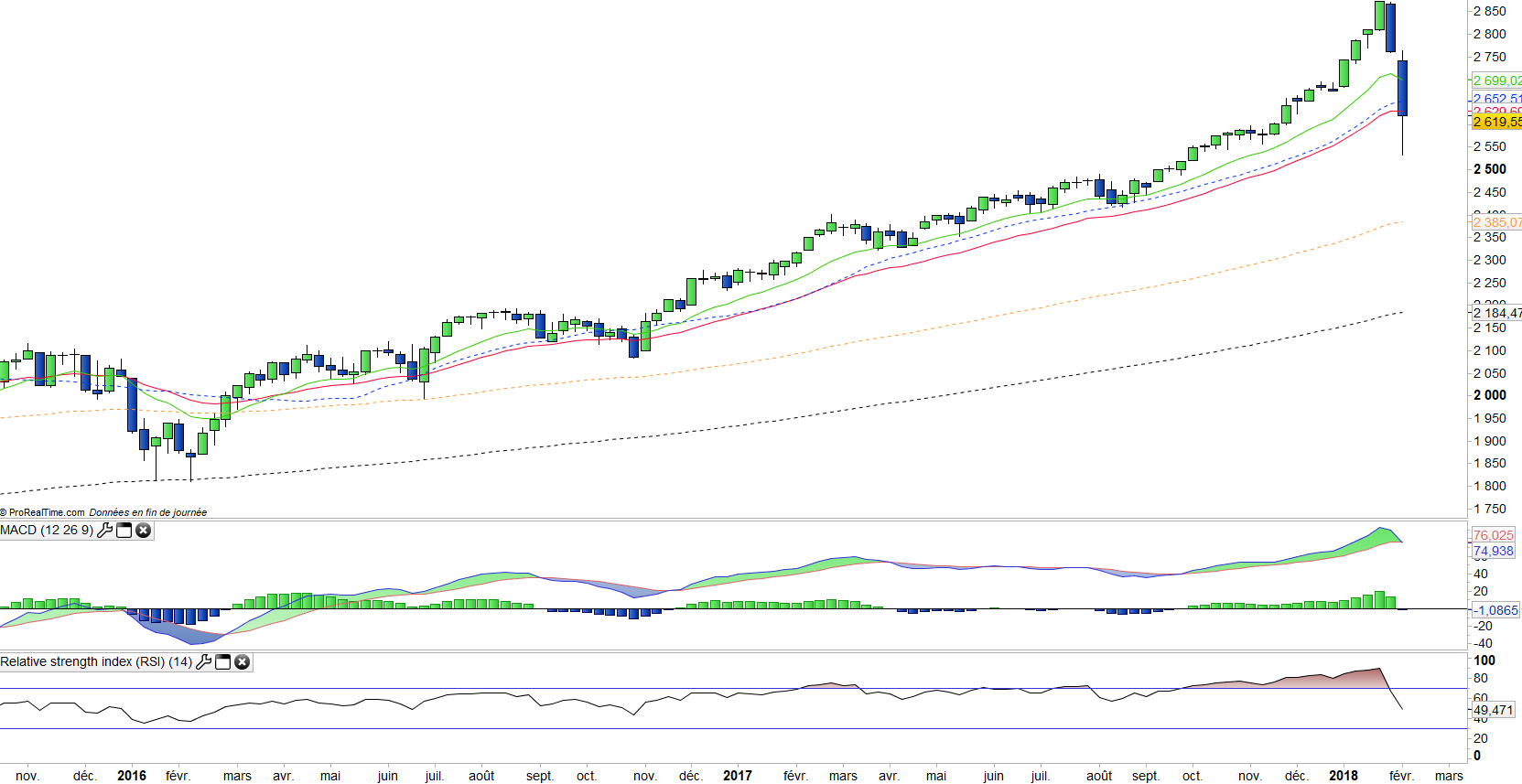

After an increase of 19.4% in 2017, and a strong January rise (+ 5.6%) the S & P500 has now entered a correction phase and has fallen by 2% since the beginning of the year.

The correction is due to fears of the return of inflation, which was triggered by the better than expected January US employment statistics on the number of jobs created and the rise in US hourly wages, which resulted in an increase in US 10-year yields to 2.85%, up from 2.45% at the beginning of the year. The absolute level of long rates is not a problem, but the speed of the rise is one. The risk is a bond Krach, which could lead to a financial crisis with its negative effects on the debt of companies whose balance sheet is weak (High Yield compartment), which would potentially significantly increase the default rate and put the banks in trouble.

However, central banks could intervene to channel the rise in long-term rates, which could also naturally pause around 3% due to the fall in equity markets and commodities likely to weigh on growth.