The ETF L100 (Lyxor) created in 04/2007, is listed in Euro on Euronext, tracks the FTSE100 index.

FTSE100 index is composed of the 100 main English stocks representative of the main sectors, while the stocks are selected according to the importance of their market capitalization adjusted for free float. No component may represent more than 15% of the index. The ETF's fees are fairly low at 0.15% and the AUM is around € 610M. Replication is indirect (via swap) and there is a policy of dividend capitalization.

Alternative ETFs: ISF ( iShares in GBP), VUKE ( vangard, in GBP), C1U ( Amundi in Euro)

Index & components

The ETF L100 (Lyxor) is quite deep, and above all fairly balanced from a sectoral point of view. The oil and gas and mining sectors together account for nearly 25% of the index (compared with 6% for the stoxx600). 19%) and consumer goods (18%). The health sector is also very important and represents 10% of the index. All this implies that the FTSE 100 is very "dollarized" because the income of these companies is usually largely realized in the US currency, which is not insignificant either given the current weakness of the dollar against the Euro. The FTSE 100 is of course quoted in sterling, so there is a particular exposure to the British currency on L100 which quotes in euros, which naturally deviated fromthe FTSE100 index for some time for these reasons.

If the "Brexit" has not turned into financial stress or banking or stock market panic, it must be said that the transmission belt of the shock was the British currency which has since fallen by about 20% against the Euro and to the Dollar. The effective exit from the United Kingdom, the 6th world economy, is expected to occur in early 2019, as the triggering of Article 5 was achieved as planned in March 2017. Its effects are likely to be felt in the long term as it is likely to require an adaptation of the English model. An extension of the negotiation period (with the preservation of the status quo) by an additional 2 years is also not to be excluded, especially if the negotiations are moving towards an agreement, which is not yet the case at present.

Europe is for the moment united against England, and is firm on its demands, while threats of dislocation from the United Kingdom begin to appear (reunification of Ireland under European flag and Scottish referendum). On the other hand, the short-term good news of the fall of the pound for English exporters could have had later on negative counterparts, such as inflation and rising interest rates, as the BOE has just pointed out.

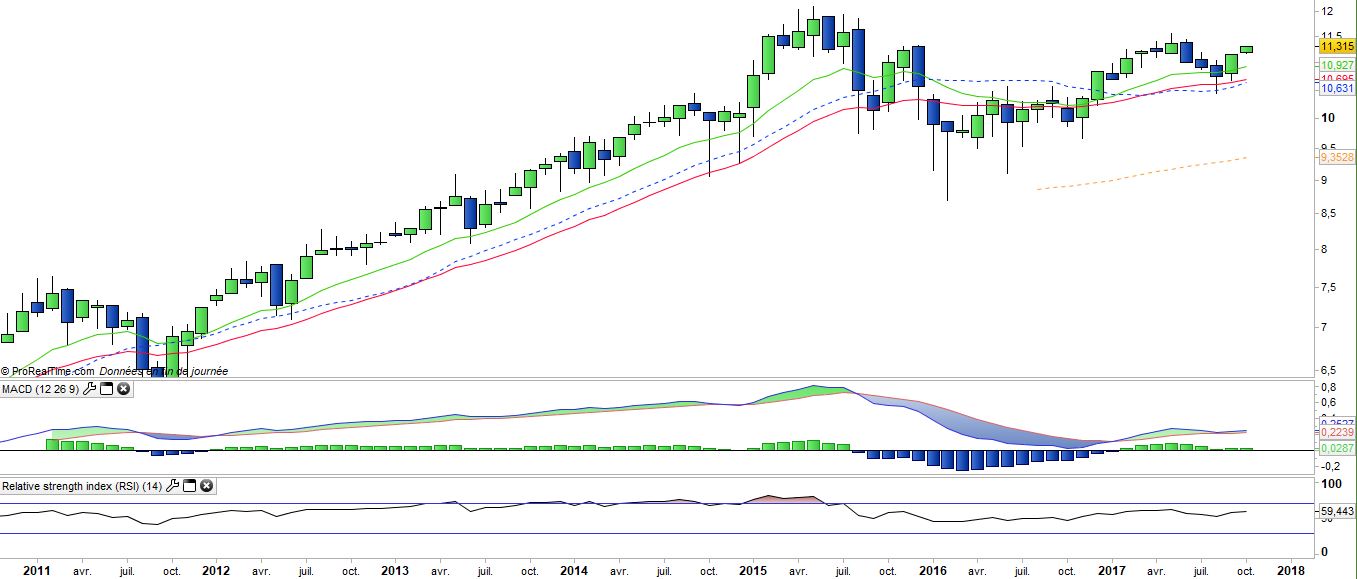

Latest developments

For the time being the English index is very resilient (+ 4.5% since the beginning of the year), but lags behind the performance of the Eurostoxx50 (+ 9.5%) despite the recent rise of raw materials, reflecting first of all the appreciation of the Euro / GBP (+ 4.4%). However, the British economy seems to be far from crumbling: unemployment is at its lowest level since 1975 at 4.4% of the active population, while manufacturing activity remains very solid (PMI higher than expectations) boosted by exports.

However, the BOE has left little doubt about its willingness to raise rates, which could change the dynamics of growth in Britain, or even bring it into a recession. At the political level, discussions with the EU remain chaotic but a more pragmatic approach is being developed on the English side, which could lead to an extension of the 2-year negotiation if sufficient mutual concessions are made here before early 2019. The worst is not certain.